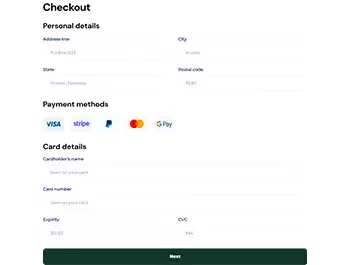

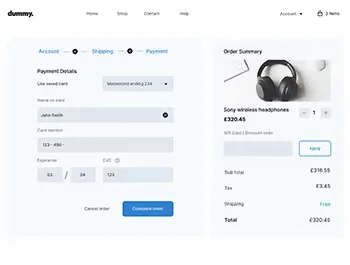

Website Payments

Card processing through your website's checkout - hosted pages, embedded checkouts, or platform plugins for Shopify, WooCommerce, and similar stores.

- Suits ecommerce, direct-to-consumer brands, and subscription stores.

- Hosted, embedded, and platform-plugin routes to fit your build.

- Rates from 0.5% when well matched to the right acquirer.